In 2026, Brussels has reason to celebrate. Russia's share of EU gas imports has fallen from 45% to 12%. Russian coal has virtually disappeared. Russian oil is down to 2% of the European market. Officials call it one of the fastest energy transformations in modern European history.

But Russian LNG is still flowing. The EU paid Russia €7.2 billion for it in 2025—enough to fund roughly five years of Iskander-M ballistic missiles at the rate Russia ordered them for 2024–2025.

As President von der Leyen stated this week, EU sanctions are aimed at weakening the economic foundations of Russia's war effort. For Ukrainians, this reality is painfully tangible: every euro of revenues from Russian fossil fuel exports is transformed into drones and missiles that strike our cities and civilians.

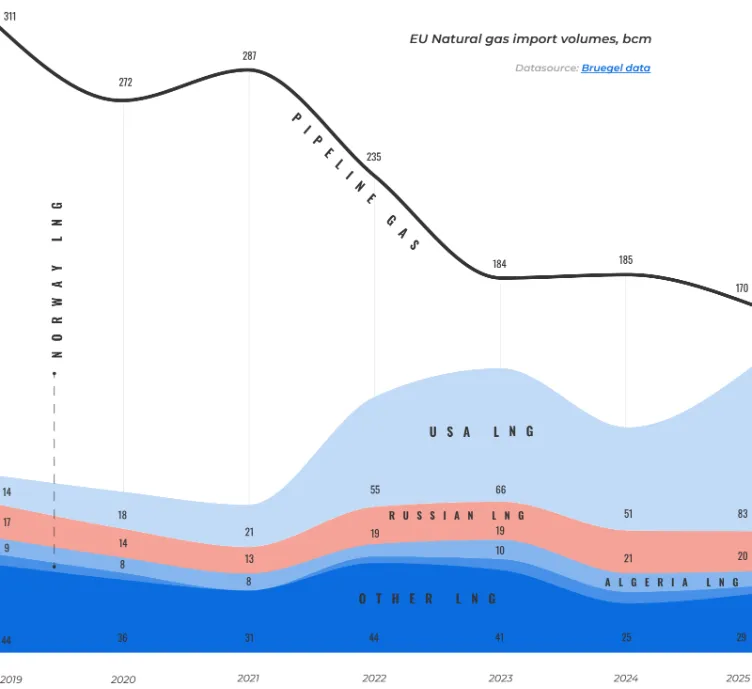

Razom We Stand's new analytical paper, Europe's Break from Russian Fossil Fuels, reveals the gap inside the celebration. Pipeline volumes collapsed, yet the LNG channel never closed. In 2025, the EU imported around 20 bcm of Russian liquefied natural gas, and imports rose. By the first quarter of 2026, Europe was receiving 97% of exports from Russia's Arctic Yamal LNG project.

Russia is being paid by Europe's choice, not contract necessity, until 2027

The EU's 19th sanctions package, adopted in October 2025, set 1 January 2027 as the legal end of Russian LNG imports under long-term contracts. The same package gave EU buyers force majeure cover to exit early.

Yet, only after four years of Russia's invasion did the German government ask SEFE, which holds a 2.9 million-tonne-per-year contract originally running to 2040, to consider invoking the legal exit available to it. Four years of civilians killed daily by Russian missiles and drones, and four years of Ukrainian soldiers holding off the world's #2 army funded by the very money earned by selling LNG to Europe.

SEFE is, as of recent reporting, still weighing the costs. The flow continues.

Specific European companies anchor this trade. France's TotalEnergies holds a 20% equity stake in Yamal LNG and the largest single offtake contract. Germany's SEFE and Spain's Naturgy hold long-term offtake contracts. Belgium's Fluxys operates the Zeebrugge terminal that handles a significant share of trans-shipment. The Yamal ice-class tankers that move the cargo are operated by Seapeak Maritime Glasgow in the UK and Dynagas in Greece.

France led EU buyers in 2025—87 ships delivering 6.3 million tonnes through Dunkirk and Montoir, worth €3.16 billion to Russia.

The TotalEnergies CEO has been candid about the philosophy. Asked about the ethics of profiting from Russian LNG amid sanctions on Russia, Patrick Pouyanné told reporters: "This is not Russian money—it's a European contract."

In February 2026, after the 20th sanctions package gave TotalEnergies additional legal protections, Pouyanné announced the contract might be terminated earlier than its 2041 end. The 20% equity stake in Yamal LNG isn't part of that timeline.

Sanctions taken hostage to restore flow of Russian oil

The oil channel tells a similar story. The April 2026 resolution of the Druzhba crisis allowed the 20th EU sanctions package and the €90 billion EU loan for Ukraine to pass—but the resolution restored Russian crude flows to Hungary and Slovakia. Ukraine, under pressure to unlock both, repaired the pipeline that Russia had struck at Brody in January and resumed transit of Russian oil through its territory.

The two countries continue importing through Druzhba's southern leg under exemptions with no defined end date. Hungary and Slovakia imported a combined 8.7 million tonnes of Russian oil in 2024—more than before the full-scale invasion.

Croatia's Adria pipeline (JANAF) can cover their oil needs. The reason it doesn't: Hungarian state oil company MOL reports approximately 30% additional profit from arbitraging Russian crude prices.

The problem is no longer willingness. The April hostage demonstrated how Kremlin-aligned EU governments can use Russian fuel exemptions as leverage on sanctions and aid. The pattern can repeat anywhere those exemptions remain.

Russia cut its own pipeline gas exports to the EU

Even the pipeline gas drop owes more to Russia than to Europe. Razom's analysis credits Russia's own export cuts—driven by Gazprom's pivot to Asian markets and the loss of the Nord Stream pipelines—as the primary cause of the collapse from 45% to 12%. Brussels accepted the result and took credit.

The diversification story is also less than it appears.

As Russian pipeline gas declined, the EU sharply increased LNG purchases—primarily from the United States. American LNG accounted for around 28% of Europe's total gas imports in 2026 and nearly 60% of all LNG consumed in Europe.

Since 2022, the EU has commissioned twelve new LNG terminals and six expansion projects, adding more than 70 bcm of import capacity.

Total LNG import capacity now stands at approximately 250 bcm per year—more than double current LNG imports. This shift now operates under the political conditions of a US administration that has explicitly used European LNG dependency as a trade and diplomatic lever. Europe has traded Kremlin leverage for White House leverage.

Closing the actual remaining channel requires enforcing what the 19th sanctions package set in October 2025—and extending it.

The package made Russian LNG imports under long-term contracts legally void from 1 January 2027 and gave EU buyers force majeure cover to exit early. EU buyers should invoke that cover now, not next year. Germany waiting until November 2025 to press SEFE is the model failure to avoid.

The 2027 deadline should also move forward. Each month of activation delay means more euros flowing to Moscow while Ukraine fights weapons funded by that revenue.

Coordinated G7 sanctions across the entire Russian LNG value chain—Novatek, Yamal LNG, Arctic LNG 2, the affiliated entities and executives, the transshipment operators, the tanker operators, the insurers. The UK has banned shipping services. The EU has not.

EU sanctions on the European companies sustaining the trade: TotalEnergies, SEFE, Naturgy, Fluxys, Seapeak Maritime Glasgow, Dynagas. And separate treatment for equity stakes—TotalEnergies plans to keep its 20% in Yamal LNG even after the contract ends. The structure outlasts the contracts.

For pipeline oil—a firm deadline on the southern Druzhba exemption. For pipeline gas—termination of the Hungary–Gazprom long-term contract for 4.5 bcm annually delivered via TurkStream, replacement with non-Russian suppliers such as Romania's forthcoming Neptun Deep project, and strengthened market monitoring to prevent circumvention through third countries.

Why is the EU moving so slowly?

The ultimate reason is that Europe still perceives the phase-out of Russian fossil fuels primarily as an economic challenge, while Ukraine experiences it as a matter of security and survival. Therefore, the business interests and lobbies of oil and gas giants and their long-term contracts with Russia get priority over cutting off Russia’s war revenue immediately and completely and establishing the continent’s energy independence.

The deeper truth behind all of this is one Russia's war has made unmissable. Fossil fuel dependence creates leverage for whoever controls the supply. Replacing the Kremlin with Doha or Washington reduces immediate risk but preserves the structure. The only path that ends the leverage is reducing demand—through renewables, electrification, heat pumps, and grids.

The EU has already proven this works. Since 2022, gas consumption has fallen 15–18%, driven not by new LNG terminals but by efficiency and renewables. Wind and solar rose from 17% to 29% of the electricity mix. Solar capacity nearly tripled, from 120 GW to 338 GW.

That is the foundation. Finishing the job means matching the speed of demand reduction with the speed at which Brussels closes the LNG channel still funding Russia's war.

Europe has nearly broken from Russian fossil fuels. The "almost" means contracts still active until 2027, equity stakes that outlast them, named companies still buying, money still flowing to Moscow. Closing that gap—without falling into the next dependency—is the work left.

The lobbying to bring back Russian gas is back. Faster electrification is the answer

Editor's note. The opinions expressed in our Opinion section belong to their authors. Euromaidan Press' editorial team may or may not share them.

Submit an opinion to Euromaidan Press