When oil prices jump, the standard explanation follows quickly: supply fell, demand rose, prices climbed. It sounds tidy. It is also wrong, or at least badly incomplete.

The market is asking: what if the barrels cannot reach buyers tomorrow?

Oil is not priced like potatoes at a village market. It is priced more like a forward-looking risk, almost like insurance. The market is not just asking how many barrels exist today. It is asking: what if those barrels cannot reach buyers tomorrow?

Fear has a price tag

The US Energy Information Administration (EIA) notes that oil prices respond not only to current supply and demand but also to expectations, uncertainty, inventories, and potential disruptions.

Geopolitical events can raise volatility even without an immediate physical shortage—and when spare production capacity is low, a “risk premium” enters the price even before production falls by a single barrel.

Iran declared the strait shut and warned it would fire on any vessel attempting to transit.

Brent crude rose from $71 per barrel on 27 February to $94 by 9 March—and was trading near $99 by 13 March—even as physical damage to oil infrastructure remained limited. The EIA found the Strait of Hormuz “effectively closed to most shipping traffic” not by a physical blockade, but by threat: Iran declared the strait shut and warned it would fire on any vessel attempting to transit.

According to Reuters, about 150 tankers had dropped anchor in and around the strait, with marine insurers cancelling war-risk cover or raising premiums fivefold.

Munro Anderson of marine war insurance specialist Vessel Protect called it “a de facto close of the Strait of Hormuz, based primarily around perception of threat rather than a tangible blockade.”

If a fifth of the world’s oil and LNG passes through one 39-kilometer-wide chokepoint, the price of a barrel is never just the price of extraction.

If a fifth of the world’s oil and LNG passes through one 39-kilometer-wide chokepoint, the price of a barrel is never just the price of extraction. It is also the price of transport, political stability, naval security, and confidence that the next cargo will arrive. Once that confidence breaks, the market starts paying up in advance.

History keeps repeating

The pattern is not new. The Arab oil embargo of 1973 sent prices quadrupling within months, before Western drivers faced a physical shortage. Iraq’s invasion of Kuwait in August 1990 produced an immediate price spike on the day of the attack, not when supply actually tightened.

Each time, the mechanism was the same: expectations moved first, oil itself second.

Drone strikes on Saudi Arabia’s Abqaiq processing facility in September 2019 drove one of the sharpest single-day jumps in years, even though production recovered within weeks. Each time, the mechanism was the same: expectations moved first, oil itself second.

The country with no cushion

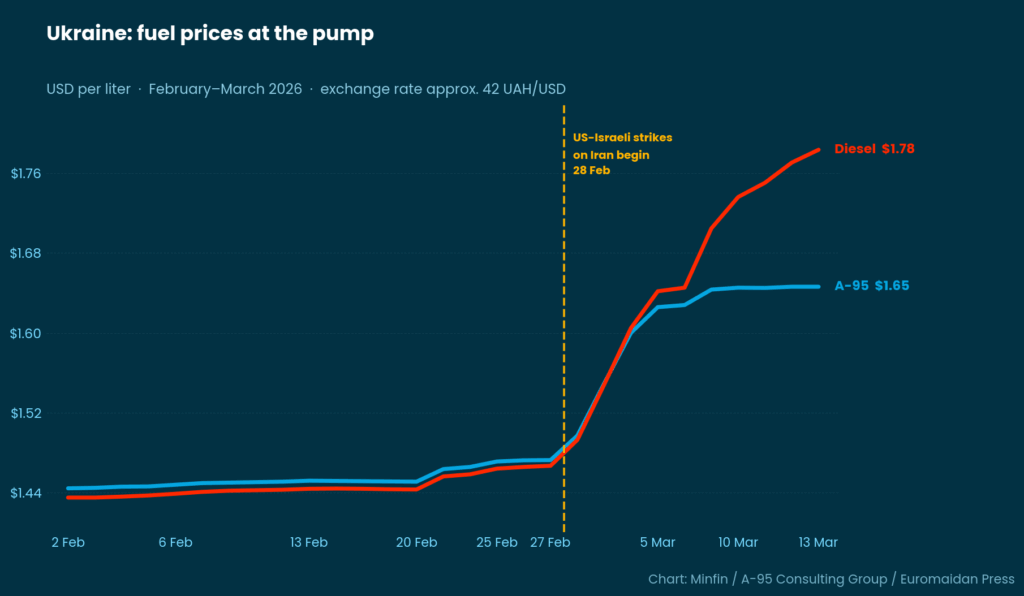

Ukraine has almost no cushion between global oil fears and the pump. Russia struck the Kremenchuk refinery—then Ukraine’s largest, with an annual capacity of 18.6 million tonnes—first time already in April 2022, and subsequent strikes have more or less eliminated what remained, leaving Ukraine importing roughly 85% of its fuel.

In oil, the real contest is usually over expected future scarcity.

When global oil prices spike, Ukrainian drivers feel it almost immediately. Fuel prices rose by 6–10 hryvnias ($0.14–$0.24) per liter in the days after the Hormuz disruption—a jump of about 10–15% at the pump.

In that sense, supply and demand do set the floor. But in oil, the real contest is usually over expected future scarcity. The market is not just buying barrels. It is buying protection against being left without them.

Editor's note. The opinions expressed in our Opinion section belong to their authors. Euromaidan Press' editorial team may or may not share them.

Submit an opinion to Euromaidan Press