Russia’s gold reserves—built over decades to outlast Western sanctions—sank to their lowest level since March 2022 last month, while the Middle East war, now pushing Urals crude past $100 a barrel, has cut the price of gold by 27% since January. Moscow is being forced to sell its emergency reserve at a steep discount, by a conflict it had no hand in starting.

The 500,000-ounce drop over two months is the steepest since 2015.

The Central Bank of Russia held 74.8 million troy ounces of gold on 1 January, but only 74.3 million troy ounces, or 2,310 metric tons, in February. The 500,000-ounce drop over two months is the steepest since 2015.

The oil windfall from the Middle East conflict generates as much as $150 million in additional daily revenue for Moscow’s budget. Urals crude has surged 71% over the past month to $100.23 a barrel.

The hedge that wasn’t supposed to move

For the first time since 2002, Russia has begun selling gold from its international reserves, having started on the domestic market in November 2025 to plug a deficit that had ballooned to 20 times the previous year’s level.

The central bank sold about 15 metric tons in January and February combined—the largest two-month drawdown since Q2 2002, when Russia’s reserves fell by almost 40 tons, according to the World Gold Council.

By January 2026, Ukraine’s Foreign Intelligence Service (SZRU) said Russia planned to liquidate nearly $19 billion from gold and precious metal reserves in the first six months of the year alone. The National Wealth Fund’s gold holdings had by that point collapsed from over 550 tons in 2022 to roughly 160 tons.

At the same time, Moscow is protecting its yuan reserves—its only remaining tool for currency interventions.

The fund’s liquid assets stood at $51.8 billion as of 1 March—down from $55.8 billion a month earlier and less than half the $113 billion held before Russia’s full-scale invasion of Ukraine.

At the same time, Moscow is protecting its yuan reserves—its only remaining tool for currency interventions after roughly $300 billion in reserves were frozen by Western sanctions—leaving gold as the asset of last resort.

Gold peaked and then collapsed

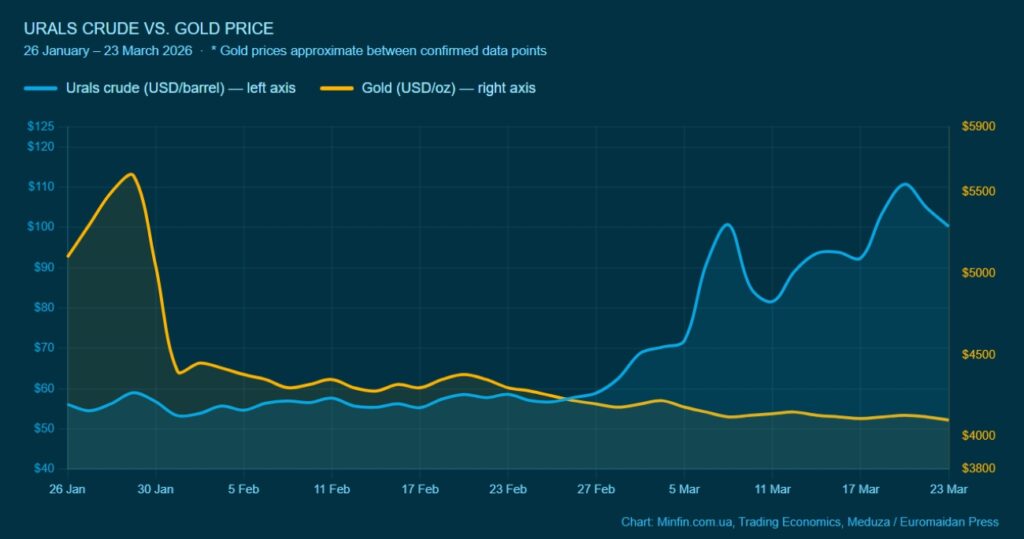

Gold offered Moscow a partial cushion. Prices hit $5,600 per ounce in January 2026—a record high—as investors fled the dollar amid fears of US trade wars.

Then on 30 January, gold fell nearly 10% in a single session after US President Donald Trump nominated Kevin Warsh as Federal Reserve chair—a pick markets read as a signal of dollar stability, triggering a global sell-off in precious metals. By 23 March, gold had fallen to $4,100 per ounce, its lowest since late November 2025.

US and Israeli strikes on Iranian territory pushed investors out of gold and into energy.

Trending Now

US and Israeli strikes on Iranian territory from late February compounded the pressure. They sent Urals prices surging nearly 70% in three weeks—the same shock that pushed investors out of gold and into energy at the moment Russia most needed prices to hold.

Two prices, opposite directions

Russia’s oil revenues—battered throughout 2025 by sanctions and collapsing prices—are recovering sharply thanks to a conflict Moscow plays no part in shaping. Urals crude stood at $100.23 a barrel on 23 March, $41 above the $59 per barrel assumed in Russia’s 2026 budget.

Vladimir Chernov, an analyst at Freedom Finance Global, a Kazakhstani brokerage firm, told The Moscow Times that every $10 increase in oil prices delivers $1.6 billion in additional monthly revenue for Moscow’s budget—putting the current windfall at over $6 billion a month.

Moscow can slow gold sales if oil prices stay high—but both prices are driven by forces outside the Kremlin’s control.

Russia’s cumulative federal deficit for 2022–2025 exceeded 15 trillion rubles ($183 billion); in the first two months of 2026 alone, another 3.5 trillion rubles ($43 billion) were added to it.

The US Institute for the Study of War assessed on 23 March that the Middle East conflict “is likely exacerbating Russia’s ability to resolve its liquidity problems related to its unsustainable wartime spending.”

Moscow can slow gold sales if oil prices stay high—but both prices are driven by forces entirely outside the Kremlin’s control, and right now they are moving in opposite directions.