Ukraine’s central bank held its key rate at 15% on 19 March, pausing a series of planned cuts launched only in January and signaling readiness to raise rates if Middle East energy prices keep driving inflation above forecast.

Imported pressure

The Iran war arrived before the second cut could come. Crude oil prices surged more than 40% after the conflict escalated, reaching Ukrainian consumers within weeks.

Fuel inflation hit 8% year-on-year in February, its sharpest acceleration in months, pushing the consumer price index (CPI)—the broadest measure of what Ukrainians pay for goods and services—to 7.6% overall, slightly above the NBU’s January projections.

Ukrainians’ expectations for future prices worsened sharply as fuel and raw food costs rose simultaneously.

The NBU now projects the trajectory will run higher still in the months ahead. Core inflation (which strips out volatile fuel and food prices) is holding exactly on forecast at 7%, showing that domestic price dynamics remain under control. But Ukrainians’ expectations for future prices worsened sharply as fuel and raw food costs rose simultaneously.

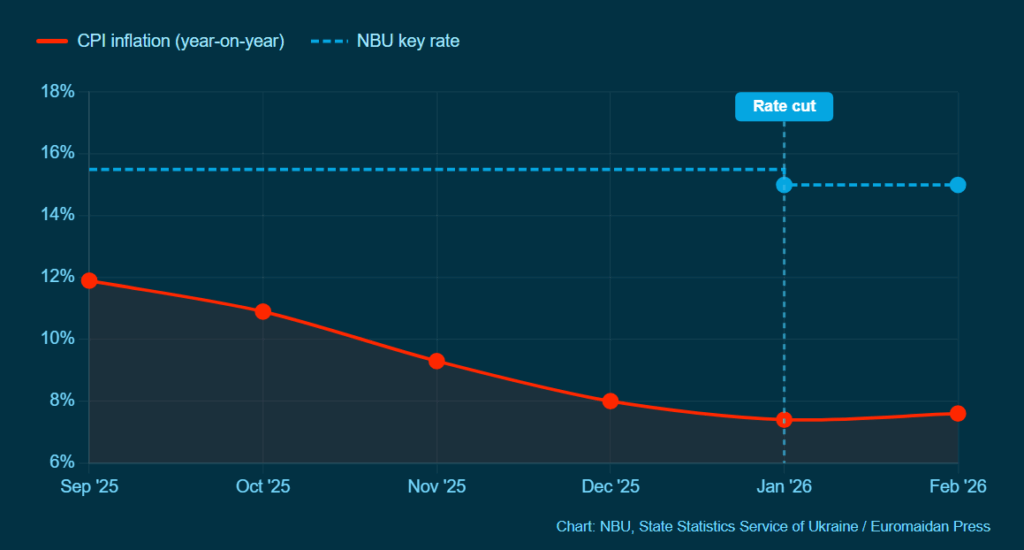

That matters because January was supposed to mark the start of a sustained easing. The NBU launched its rate-cutting cycle on 29 January, cutting from 15.5% to 15%—its first reduction since March 2025—as inflation fell to 8% year-on-year in December and the EU’s €90 billion ($94 billion) support package for 2026–2027 eased fears about external financing. Further cuts were built into the bank’s own projections for the year.

If inflationary risks persist, rates will hold; if they intensify, the bank is prepared to raise them.

The January projections—under which those further cuts had been planned—were “not materializing at this time,” NBU governor Andriy Pyshnyy told Kyiv Post. He added that if inflationary risks persist, rates will hold; if they intensify, the bank is prepared to raise them. Whether rates fall further this year now depends on a war Ukraine isn’t fighting.

The same oil shock freezing Ukraine’s rate relief is simultaneously filling Russia’s war budget—delivering up to $150 million a day in additional revenue and partially reversing months of Western sanctions pressure.

Trending Now

$55 billion to hold the line

According to the NBU’s 19 March statement, Ukraine received $5.5 billion in official external financing in the first two months of 2026, keeping international reserves at approximately $55 billion at end-February—a level the bank said gives it ample capacity to defend exchange rate stability.

The hryvnia has weakened against the dollar in recent weeks, alongside most global currencies, driven by geopolitical uncertainty.

The hryvnia has weakened against the dollar in recent weeks alongside most global currencies, driven by geopolitical uncertainty; against the euro and Ukraine’s main trading partner currencies, the move has been modest.

Lending continues to grow above 30% year-on-year, Pyshnyy noted, meaning January’s cut is passing through to the real economy and the March hold will not reverse it.

The next rate decision is 30 April—a date that will say as much about the Middle East as about Ukraine.