This recovery process is accompanied by a general stabilisation trend. The exchange rate has been stable for a considerable amount of time and is now backed by significantly larger foreign exchange reserves. Inflation is still high at currently 15.6%, but will decrease significantly this and next year. Thanks to the fact that the Naftogaz deficit has been eliminated, the budget deficit amounted to only 2.2% of GDP in 2016. However, expenditures for the recovery of the banking sector amounting to 5.4% of GDP are not included in the budget. Nationalising the country’s largest bank was, without doubt, a necessity.

In spite of these economic policy success stories, economic growth is with a meagre 2% far below potential. The speed of reforms has to be significantly accelerated in order to achieve tangible improvements for the population, thus securing its further support for the reform process

Investment supports economic growth

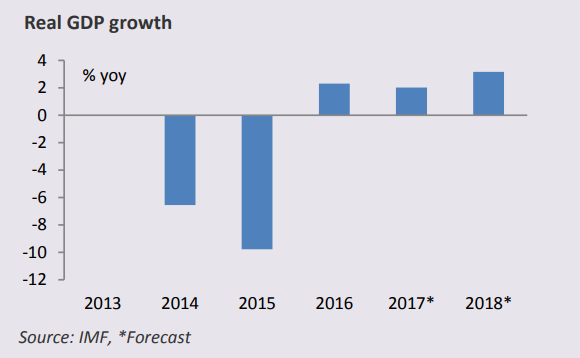

After the heavy crisis in 2014/15 the Ukrainian economy grew by 2.3% in 2016. In 2017, the recovery continues; GDP is forecast to increase by 2.0%. On the demand side, this trend is mainly driven by increasing investment – especially in agriculture. Investment increased by 18% in 2016 and by 20% in the first quarter of 2017. On the supply side, agriculture is a key factor. It grew by more than 6% in 2016; production and export of grain reached record levels. The industrial sector, being the most important one, also recorded positive growth (2.4%) for the first time since 2011.

The fact that economic growth is slowing down in 2017 compared to the previous year can mainly be attributed to the trade blockade in the Donbas. In the area not controlled by the government of the country several enterprises have been seized in March 2017. In response, the government officially stopped trade with this area. This dampened economic growth by 1.3%. The GDP reduction mainly relates to the energy and steel industry and will diminish over time.

Stable exchange rate and increasing external trade

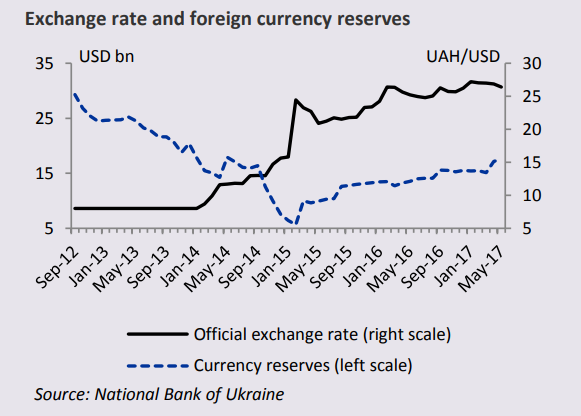

Stabilisation continues also in the external sector. The flexible exchange rate develops smoothly since 2015, with a positive impact on confidence. Also foreign exchange reserves increased thanks to international credits and interventions on the foreign exchange market, and are currently at their highest level since 2014 (USD 18 bn in June 2017).

This enabled the National Bank to gradually loosen the foreign exchange restrictions introduced during the crisis. Thus, dividends from 2014/15 can gradually be transferred abroad since June 2016 and since April 2017 also dividends from 2016. Furthermore, Ukrainian exporters have to exchange “only” 50% of their foreign exchange proceeds in Hryvnia instead of 75% earlier.

A positive trend can also be observed in external trade: After four years in a row of decreasing exports, they are expected to increase by around 9% in 2017. The main reason for this is the recovery of international commodity prices. Also imports will grow significantly this year – by almost 11%. This development reflects higher investment in the context of economic recovery.

National Bank brings inflation under control

Inflation has been decreasing since 2015. Although the current value of 15.6% in June 2017 is again slightly higher than the level at the end of 2016, the National Bank has in general regained control of the price development. It is expected that inflation will continue to decrease gradually in this year and the next. Accordingly, the National Bank has continuously reduced its policy rate: While it amounted to 30% in June 2015, its current level is at 12.5%. It can be expected that this will have a positive impact on lending, although other factors like the protection of creditors’ rights play a more important role for lending.

The National Bank has also conducted a successful reform of the banking sector: The former Governor Gontareva accomplished a good job in thoroughly cleaning up the sector, which led to the closure of 87 banks. The country's largest bank, Privatbank, was nationalised. After Gontareva has paved the way for a positive development of the banking sector in the long run, she quit her job at her own will. The question about her succession still remains to be answered.

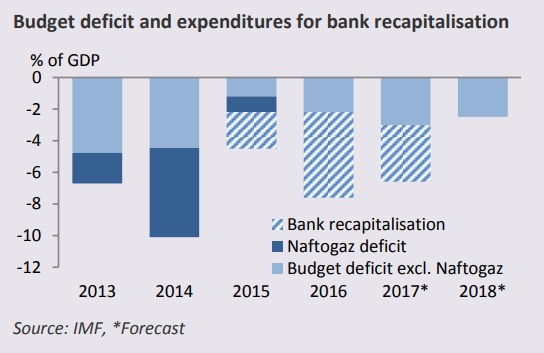

Public finance: After Naftogaz comes Privatbank

In 2016, the budget deficit was lower than agreed with the IMF, amounting to 2.2% of GDP. The deficit of the public gas provider Naftogaz, which had amounted to 5.6% of GDP in 2014, could even be completely eliminated. Both developments can be assessed positively. A new fiscal burden is, however, the already mentioned nationalisation of Privatbank at the end of 2016. The funds needed for this measure as well as other funds needed e.g. for the deposit guarantee fund or other state-owned banks amounted to 5.4% of GDP in the last year. More costs will incur in 2017.

Currently, an amount equal to 1.4% of GDP has already been identified as additionally needed funds in 2017; in total they will most probably reach 3.6% of GDP. Even though these expenditures do not count as part of the budget deficit, they are a heavy fiscal burden that leads to higher government debt.

Outlook

The Ukrainian economy is on a clear path of economic recovery that is reflected by the positive development of several economic sectors. Accordingly, the current problems around the trade blockade in the East of Ukraine have no serious macroeconomic impact: Growth has slightly slowed down this year, but this does not lead to an end of the generally positive trajectory. Furthermore, the negative impulse will diminish in the course of time as enterprises find new ways of dealing with the negative consequences. At the same time, it needs to be said that annual growth rates of 2% are too low after the heavy crisis in 2014/15, especially taking into account the vast potential of the Ukrainian economy.

A sharp acceleration of the speed of reforms is the only way to improve the living standards and thus make sure that people's willingness to support the reform process will be preserved.